Early on in 2019, I created a budget on how much money I’d spend for the year. This post shares how much money I expected to spend, what I actually spent, and my analysis of the results.

Why?

I’ve always been frugal, but have never known what my spending habits are. This budget exercise was meant to help me:

- Understand the expectations vs. reality of my personal finances

- Determine whether I can comfortably afford various leisure activities

- Gain experience in budgeting to help with future financial responsibilities such as home mortgage and family.

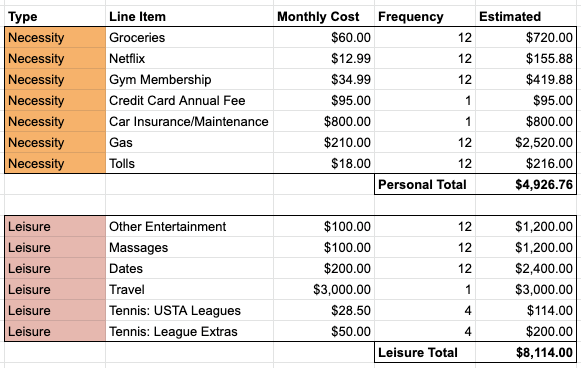

Expectations

Note 2: Netflix is “necessity” because I pay for the family account.

The budget was simple. Necessity is self explanatory. Leisure meant things that I could live without, but were things that I still wanted. Coming into the year, I wanted the following:

- Get 1-2 deep tissue massages per month

- Participate in 1 tennis league per season

- Go on 1-2 vacations

In total, I estimated spending $13,041, excluding rent and business expenses.

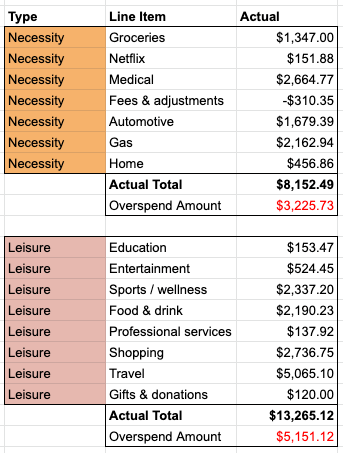

Reality

Turns out I spent way more money on things I didn’t account for.

Breakdown of Necessary Costs

Medical Costs: $0 expected vs. $2,664.77 actual. I didn’t factor in medical bills at all. My foot surgery cost over $1,700 out of pocket. I also spent about $1,000 on a glaucoma checkup. The latter was an unpleasant surprise, for I expected the bill to only be a $45 co-pay; I didn’t realize that my insurance didn’t cover the testing.

Automotive Costs: $800 expected vs. $1,679.39 actual. Owning a Japanese sedan, I had the expectation that my car would not experience any significant issues. I was quite surprised to discover that I spent 2x more on vehicle maintenance and insurance than expected. Some A/C issues and radiator issues racked up the costs.

Groceries: $720 expected vs. $1,347 actual. My company caters both breakfast and lunch. I also often take home leftovers for dinner. I therefore only expected to purchase fruits and groceries for the weekend. The biggest oversight here was the social aspect: throughout the year, I prepared food for groups of people for potlucks and get-togethers. I also purchased a decent amount of alcohol to bring to social gatherings.

Home: $0 expected vs. $456.86 actual. This was another expense that I didn’t account for at all. Having moved 8 times in 7 years, I’ve been accustomed to owning few belongings, let alone any household products. But my mentality shifted this year from on-the-go to settle-down. I ended up purchasing several household items like an Instant Pot, knife set, pots & pans, humidifier, and more. I consider these as one-time expenses and don’t them to recur in 2020.

Gas: $2,520 expected vs. $2,162 actual. I was happy to see that I spent less money on gas than expected.

recommend the card.

Fees & adjustments: $95 expected vs. ($310.35) actual. My Chase Sapphire Preferred credit card costs $95/year. Upon receiving my medical bills, I signed up for two more credit cards with sign-up bonuses. Paying for my surgery with the Bank of America Travel Rewards card gave me $200 cash back, while the Capital One SavorOne gave me $150 cash back. I also received more cash back through the Chase Offers program. Instead of an expectation of spending $95 in this category, I ended up saving over $300.

Breakdown of Leisure costs

Education: $0 expected vs. $153.47 actual. I forgot about book purchases. This amount was entirely in e-books.

Entertainment: <$1,200 expected vs. several thousand actual. This one was hard to classify. Originally, the category was to include dining, outdoor activities, event tickets, movie theaters, etc. In reality, I spent way more money than expected on dining and tennis, each which warrant separate categories on their own. The $524.45 amount reflects movie tickets, outdoor activities like kayaking, and tickets for the Silicon Valley Classic tournament.

Sports/Wellness: $1,514 expected vs. $2337.20 actual. As mentioned earlier, I wanted to get 1-2 massages a month, as well as play in recreation tennis leagues throughout the year. In reality, I spent a lot of money getting into tennis by purchasing several high-end tennis racquets and accessories such as strings, grips, and balls. In addition, practicing at private tennis courts racked up costs. Sadly, I only got 5 massages throughout the year instead of 12+.

Shopping: $0 expected vs. 2,736.75 actual. I went completely overboard here. My passion for tennis led to impulse purchases on about 10 pairs of brand name polo shirts and shorts, 4 long sleeves, and 4 athleisure jackets. Blame the Federer/Nadal/Djokovic marketing. I also updated my professional wardrobe with shoes and dress shirts. I initially felt guilt with each purchase, but am glad to say that I don’t have a single regret — all the clothes are worn regularly. Lastly, this category also includes gifts such as birthdays, anniversaries, baby showers, etc.

Food & drink: <$1,200 expected vs. $2190.23 actual. I was quite reclusive between 2013-2018, having invested all my time into work which left no extra energy to socialize. But with the aforementioned mentality shift, I’ve been the most social in years. Most of my spending in this category came from dining at restaurants, supplemented by coffee shops and bars (still don’t drink, but have bought a few rounds).

Travel: $3,000 expected vs. $5,065.10 actual. The overspending in this category was not a surprise. Many trips I took this year were spontaneous: the national park trip with my dad, Seattle/Mount Rainier, Nashville, and Hawaii were all paid for just 1-3 weeks before the travel date. Last minute travel purchases add up.

Gifts & donations. Tax deductible donations to 501(c)3 orgs such as Wikipedia or UC Berkeley.

Other Interesting Notes

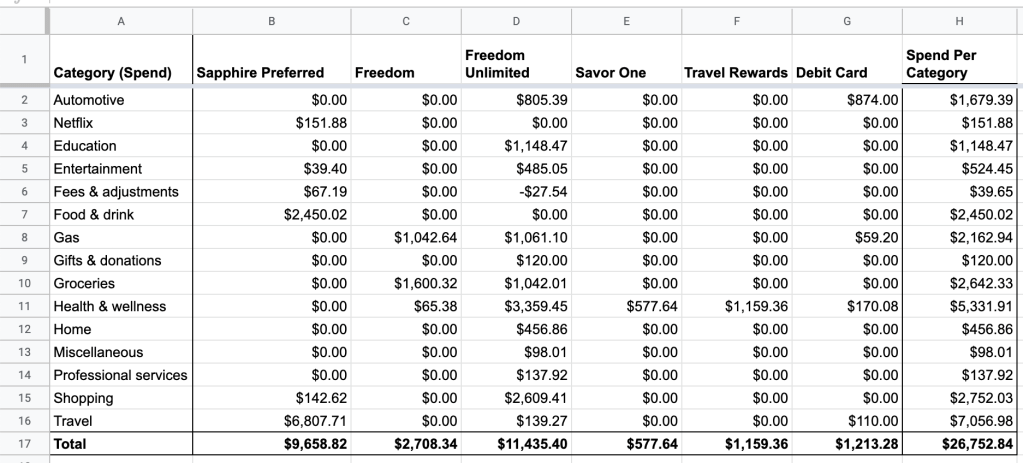

- Spent $26,752.84 across all credit and debit cards. The figure excludes rent and personal business expenses

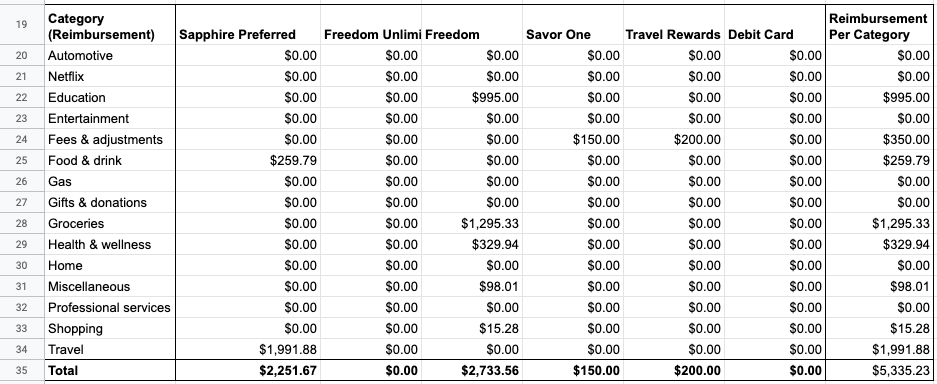

- Reimbursed $5,335.23 by work, family, or friends

- Earned 52,882 Ultimate Rewards (UR) points across four Chase credit cards

- My mom helped me earn 6,476 UR points from grocery shopping with the Chase Freedom card

Overall Assessment

I learned a lot through this exercise. This was enjoyable, and I am now in the middle of budgeting for 2020.

Subtracting reimbursements, I spent $21,417.61 in 2019. This amount was $8,376.85 more than I had planned for, demonstrating that my budget planning was poorly executed.

The good news is that many expenses are non-recurring. This includes the surgery, tennis racquets, athleisure gear, and home products. I expect my spending will be <$19,000 in 2020.

How did I track my expenses?

In general, I try to only spend money using credit cards, specifically with my four Chase cards. Chase automatically classifies each purchase into a spend category (e.g. automotive, home, health & wellness, travel). They correctly predict most of the spend categories, and I simply rectify any items that have been mis-classified.

Modeling off of Chase’s spend categories, I created a spreadsheet and populated each card’s spend into different columns. Below are the detailed results.

Note 2: I excluded rent to not disclose my rent costs.

From there, I reviewed my year-end credit card statements for transactions that I given a reimbursement, and created a separate section in the spreadsheet for it.

For example, travel reimbursements includes my employer paying me back for hotel stays and commute tolls. Education includes attending the Salesforce Dreamforce conference for work.